Pre-Payment Fraud Prevention Starts Before Funds Move

Fraud prevention expectations across the federal landscape are increasing rapidly.

Recent actions by the Federal Fraud Task Force, along with expanded payment integrity initiatives from Treasury, OMB, DOJ, and partner agencies, are increasing expectations that organizations demonstrate fraud prevention controls are operating effectively before funds are disbursed.

For years, many organizations focused primarily on recovering improper payments after funds were already distributed. That approach is becoming increasingly difficult to sustain. Accelerated funding timelines, growing oversight expectations, and more sophisticated fraud schemes are forcing agencies, grant programs, contractors, and recipients to shift their attention earlier in the process.

Today, the expectation is prevention before payment.

While the current environment may feel new, many of the underlying expectations are not. Eligibility verification, documentation, monitoring, segregation of duties, and internal controls have long been foundational principles within federal financial management and grants management. What is changing is the expectation that organizations demonstrate these controls are actively operating and supported by stronger oversight and data-informed decision making.

That means organizations must be able to:

- Verify eligibility before disbursement

- Strengthen front-end controls

- Monitor transactions continuously

- Maintain audit-ready documentation

- Demonstrate operational accountability

This is not a reinvention of compliance fundamentals. Strong fraud prevention still depends on internal controls, documentation, oversight, and disciplined execution. The difference is that organizations are now expected to operationalize those practices faster, more consistently, and at greater scale.

Prevention Works Best When It Is Built Into Operations

The most effective fraud prevention environments do not treat controls as isolated compliance activities.

They integrate prevention directly into day-to-day operations.

That includes:

- Eligibility verification before obligation or payment

- Subrecipient risk assessments

- Grant drawdown reviews

- Recipient monitoring activities

- Pass-through entity oversight

- Identity validation against authoritative sources

- Automated exception rules and transaction screening

- Segregation of duties and approval controls

- Continuous monitoring and escalation workflows

The organizations making the strongest progress are aligning policy, process, workforce readiness, and data into a single operating model.

That alignment matters because fraud prevention is rarely a technology problem alone.

Most control failures happen because:

- Processes are inconsistent

- Documentation is incomplete

- Oversight is fragmented

- Accountability is unclear

- Monitoring occurs too late in the process

Strong controls reduce risk only when they operate consistently in practice.

Data Turns Prevention into an Operational Capability

Data-driven oversight is becoming one of the most important components of modern fraud prevention.

Organizations are increasingly using analytics to identify anomalies before funds move.

That may include:

- Cross-checking identities against death records and sanctions lists

- Validating banking details and addresses

- Detecting duplicate invoices or claims

- Monitoring unusual payment velocity

- Comparing activity against peer and historical patterns

External data sources can strengthen these controls significantly.

Examples include:

- SAM.gov

- Do Not Pay

- Debarment and sanctions files

- Single Audit findings

- Office of Inspector General reports

- Agency eligibility and payment verification systems

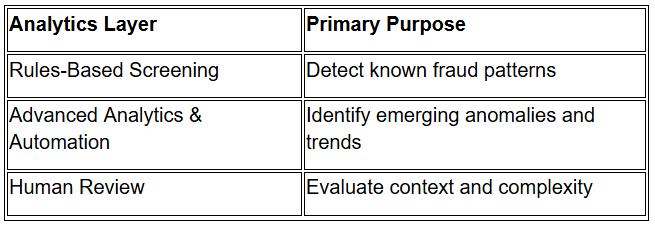

The strongest prevention programs typically combine multiple layers of review.

Technology accelerates detection.

Human judgment still determines accountability.

Governance and Workforce Readiness Matter More Than Ever

Technology alone cannot create a resilient fraud prevention environment.

Long-term success depends on governance, operational discipline, and workforce readiness.

Executive leadership plays a critical role in establishing prevention as an operational expectation rather than simply a compliance exercise.

Organizations should establish clear ownership for:

- Fraud risk governance

- Escalation protocols

- Documentation standards

- Monitoring responsibilities

- Corrective action tracking

High-performing organizations often create cross-functional oversight structures that include:

- Finance

- Grants management

- Acquisition and procurement

- IT and cybersecurity

- Program operations

- Legal and compliance

- IG liaison functions

That coordination helps organizations align policy, data, analytics, and operational oversight more effectively.

As fraud risks continue evolving, organizations should also maintain close coordination with Chief Information Officers (CIOs), cybersecurity teams, and Offices of Inspector General (OIGs), which are often monitoring emerging fraud schemes, cyber-enabled threats, and investigative trends across government.

Workforce training is equally important.

Employees responsible for payments, grants, acquisition, and monitoring activities should understand:

- How to complete pre-payment verification

- What strong documentation looks like

- How to identify fraud indicators

- When to escalate issues

- How to apply controls consistently

The strongest fraud prevention environments build accountability into daily execution.

Start With High-Risk, High-Impact Areas

Organizations do not need to modernize every process simultaneously.

The most practical approach is to begin with high-risk operational areas where preventive controls can produce measurable impact quickly.

Common starting points include:

- Vendor onboarding

- Grants and subrecipient oversight

- Eligibility determination processes

- Benefit payment programs

- High-volume federal assistance programs

- Programs identified in GAO High-Risk Reports

- Beneficiary eligibility verification

- Purchase card activity

- High-volume payment environments

Early improvements often include:

- Independent banking verification

- TIN/EIN validation

- SAM and Do Not Pay checks

- Duplicate-payment detection

- Centralized exception workflows

- Stronger approval controls

These measures help organizations move reviews earlier in the payment lifecycle, where prevention is far more effective than recovery.

Back to Basics Still Matters

While data analytics, automation, and AI continue evolving, the core elements of fraud prevention remain unchanged:

- Strong internal controls

- Clear accountability

- Risk-based oversight

- Effective documentation

- Consistent monitoring

The Federal Fraud Task Force is not introducing entirely new concepts. Rather, it is increasing expectations that organizations consistently execute and demonstrate these foundational practices.

Documentation Is Still One of the Strongest Controls

Increased oversight pressure is making documentation more important, not less.

Organizations must be able to demonstrate that:

- Controls operated as intended

- Decisions were justified appropriately

- Exceptions were reviewed consistently

- Monitoring activities occurred as required

Strong documentation standards should include:

- Clear approval records

- Version control

- Standardized checklists

- Decision memos for high-risk actions

- Retention practices aligned to policy and regulation

In high-risk environments, undocumented work creates operational exposure.

If organizations cannot demonstrate what occurred, oversight bodies may conclude the control did not operate.

AI and Automation Can Support Prevention, But They Cannot Replace Discipline

Organizations are increasingly exploring AI, automation, and robotic process automation to strengthen fraud prevention.

While AI and automation are receiving significant attention, organizations should not lose sight of the fundamentals. Technology can strengthen fraud prevention efforts, but it cannot compensate for weak internal controls, poor documentation, unclear accountability, or inconsistent oversight.

These technologies can help accelerate:

- Identity verification

- Duplicate detection

- Transaction screening

- Exception routing

- Anomaly identification

But technology cannot compensate for weak processes.

Poor governance, fragmented data, unclear controls, and inconsistent documentation will still produce poor outcomes, even in highly automated environments.

The most effective organizations layer technology on top of:

- Well-designed workflows

- Validated data

- Clear accountability

- Defined escalation paths

- Disciplined operational oversight

Technology scales good processes.

It also scales weak ones.

Prevention Becomes Sustainable Through Continuous Monitoring

Fraud prevention is not a one-time implementation effort.

As agencies continue issuing updates, guidance, and collaborative fraud prevention initiatives, organizations should expect oversight expectations to continue evolving. Federal employees, grant recipients, pass-through entities, and subrecipients should remain engaged with guidance from OMB, Treasury, DOJ, agency program offices, and Offices of Inspector General.

It requires continuous monitoring, reassessment, and adjustment.

Organizations should routinely evaluate:

- Control effectiveness

- Exception rates

- Duplicate-payment trends

- Time-to-resolution

- Training completion

- Residual risk exposure

Monitoring should focus not only on whether controls exist, but whether they operate effectively under real operating conditions.

That operational discipline is what separates performative compliance from resilient prevention.

Go Deeper Into Fraud Prevention

Access the complimentary on-demand webinar to explore practical strategies for strengthening pre-payment controls, improving eligibility verification, expanding data-driven oversight, and building audit-ready fraud prevention programs that scale across today’s federal operating environment.

Sign Up For Our Blog